The first quarter of 2026 ended with a jolt. A gasoline-driven inflation spike, a geopolitical shock in the Middle East, and a Federal Reserve firmly on hold have reshaped the rate outlook for the rest of the year. Here in Berkeley, though, the spring market is telling its own story: tight inventory, competitive offers on well-prepared homes, and buyers who are done waiting for a rate environment that may not arrive anytime soon. In this update I will walk through the latest economic data, where mortgage rates stand today, what the national and California numbers show, and what I am seeing on the ground here in the East Bay.

The Economic Backdrop

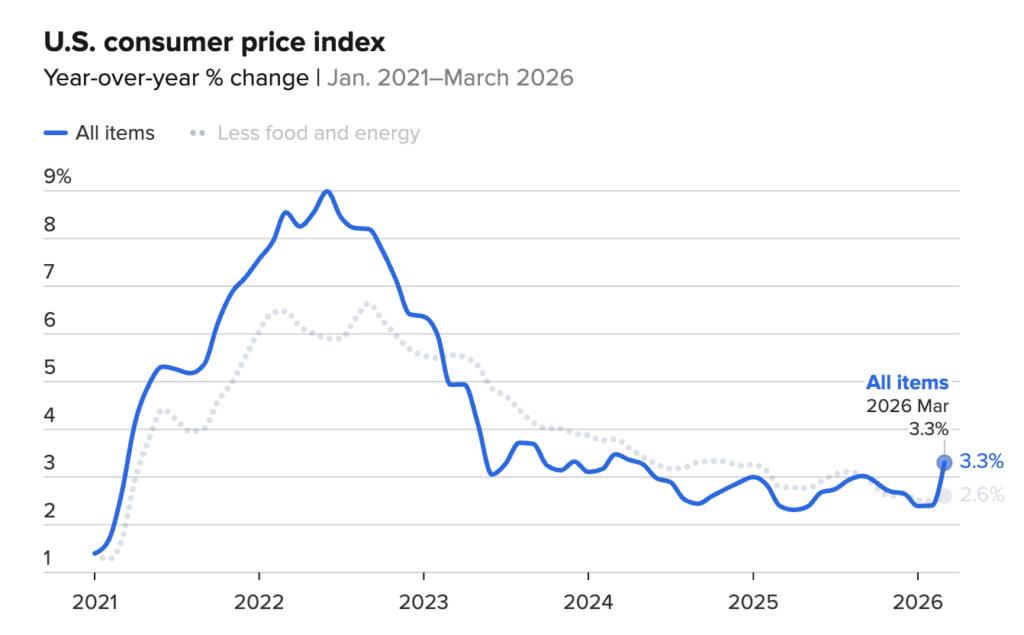

The March Consumer Price Index report from the Bureau of Labor Statistics landed hard. Headline CPI rose 0.9 percent for the month and 3.3 percent year-over-year, a sharp acceleration from February’s 2.4 percent annual reading. The culprit was energy: gasoline prices surged 21.2 percent in March alone, a consequence of the Iran conflict that upended global oil markets in early spring. Strip out food and energy, though, and the picture looks considerably calmer. Core CPI rose just 0.2 percent for the month, with the year-over-year rate at 2.6 percent. Shelter costs, long the stickiest component, rose a modest 0.3 percent. Food was flat.

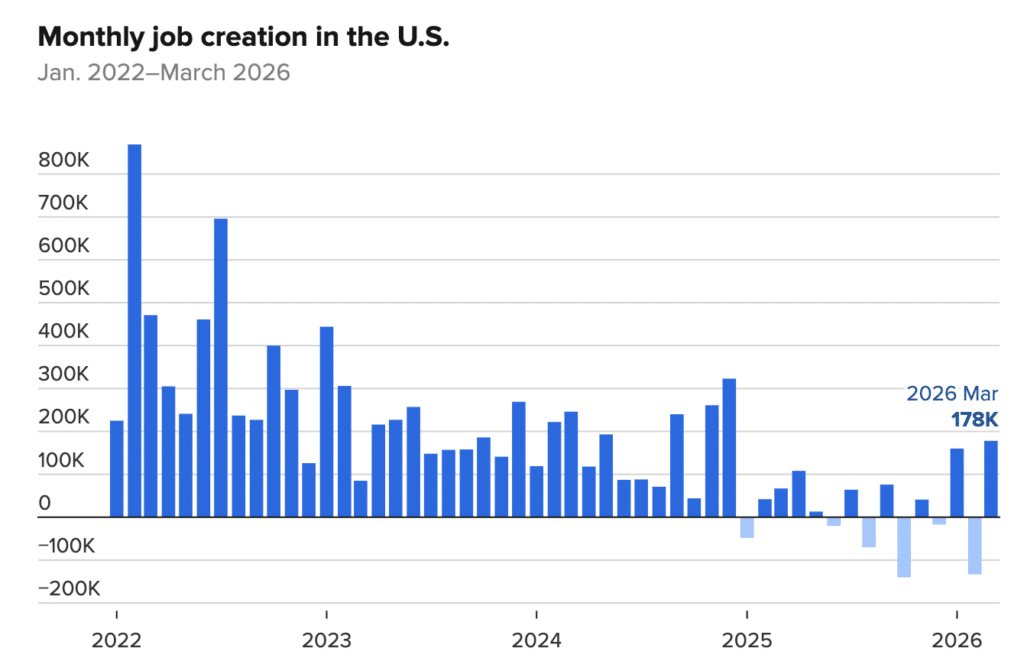

On the jobs front, the March employment report showed the economy added 178,000 nonfarm payrolls, a solid rebound from February’s revised loss of 133,000. The unemployment rate ticked down to 4.3 percent. Health care led with 76,000 new jobs, followed by construction and transportation. Federal government employment continued its steep decline, now down 355,000 from its October 2024 peak. Average hourly earnings grew 3.5 percent year-over-year, the slowest pace since May 2021, which in isolation would be welcome news for the Fed.

The Producer Price Index rose 0.5 percent in March and 4.0 percent over the year, though core PPI came in at just 0.1 percent for the month, suggesting the energy shock has not broadly infected the pipeline. At least not yet.

The Fed and Mortgage Rates

The Federal Reserve held the federal funds rate steady at 3.50 to 3.75 percent at its March meeting, with only one dissent (Stephen Miran, who preferred a 25-basis-point cut). The March dot plot projected just one rate cut for the remainder of 2026, and the meeting minutes showed several participants openly discussing the possibility of rate hikes if inflation fails to cool. The next FOMC decision comes April 28-29, and markets are pricing essentially zero chance of a cut. The takeaway: do not count on the Fed to rescue affordability this year.

The good news is that mortgage rates have drifted lower despite the Fed’s hawkish posture. The Freddie Mac Primary Mortgage Market Survey for the week of April 16 showed the 30-year fixed rate averaging 6.30 percent, down from 6.83 percent a year ago. The 15-year fixed averaged 5.65 percent, down from 6.03 percent last spring. For a Berkeley buyer purchasing a $1.4 million home with 20 percent down, a 30-year fixed at 6.30 percent translates to a principal-and-interest payment of approximately $6,950 per month. That is roughly $370 less per month than the same scenario at last April’s rate, or about $4,400 per year in savings. It matters, especially when you layer in property tax and insurance.

National and California Housing

Nationally, existing-home sales fell 3.6 percent month-over-month in March to a seasonally adjusted annual rate of 3.98 million, the lowest pace in nine months. The national median price rose to $408,800, up 1.4 percent from a year ago, marking 33 consecutive months of year-over-year gains. Inventory crept up to 4.1 months of supply, still well below the 5-to-6-month range that defines a balanced market. NAR trimmed its full-year 2026 sales forecast to 4 percent growth, down from the prior projection, citing the upward trajectory of rates. The story remains the same: not enough homes for sale, prices grinding higher, and buyers stretched thin.

California’s most recent monthly data from the California Association of Realtors covers February, showing closed sales at a seasonally adjusted annualized rate of 274,820, with a statewide median of $830,370. Median days on market was 29 days, and the sales-to-list ratio stood at 99.3 percent. C.A.R.’s full-year forecast still projects 274,400 sales and a record $905,000 median by year’s end, though escalating geopolitical uncertainty and the recent rate volatility could temper that outlook. As always, statewide California figures are a distorted lens for the inner East Bay. The mix of geographies, price points, and housing stock across a state this large means the headline rarely tells you much about Berkeley.

Berkeley: A Different Market

Berkeley’s spring market is competitive, though the data requires some nuance. Redfin MLS data for February showed a median sale price of $1.3 million with homes selling in a median of 15 days and receiving an average of six offers.

Movoto’s broader March data (which includes condos and townhomes) showed a median of $1,195,000 with 32 days on market, reflecting the wider mix of property types. The year-over-year median is down in some measurements, but that is partly a function of what has traded: a few large sales in the hills last spring skewed the comparisons. Per-square-foot prices remain solid, with Redfin showing $989 per square foot, up 7.2 percent year-over-year. Well-priced single-family homes in the flats and south Berkeley are still drawing multiple offers within two weeks. Elmwood, Claremont, and Thousand Oaks continue to see strong buyer interest, especially for updated homes under $1.5 million. The hills market above $2 million is more selective; buyers at that price point are taking their time and negotiating harder, particularly on homes with deferred maintenance or wildfire insurance complications.

BESO compliance remains a steady topic in buyer conversations. The updated Building Emissions Saving Ordinance requirements that took effect January 1 have added a new layer of due diligence for buyers evaluating older homes, and sellers who have already completed their BESO assessment and made the credit-qualifying improvements are seeing smoother transactions. I continue to advise sellers to get ahead of this before listing. On the buyer side, fire insurance availability in the hills is the other recurring question. Carriers are still pulling back from wildfire-exposed properties, and FAIR Plan premiums can add $200 to $500 per month over traditional coverage, a real cost that needs to be factored into any hills purchase.

Guidance for Buyers and Sellers

If you are buying in Berkeley this spring, the rate environment is meaningfully better than a year ago, even if it does not feel that way in the abstract. A half-point improvement on a $1.12 million loan translates to real monthly savings. Do your homework before you start touring: get fully underwritten, know your monthly number, and understand the full cost picture including transfer taxes, insurance, and any BESO-related work. My buyer net sheet calculator and mortgage calculator are built specifically for Berkeley transactions and can help you model the numbers before you write an offer.

For sellers, pricing strategy matters more than ever. Homes that are well-prepared, properly staged, and priced to the market are still generating competitive offers and closing quickly. Overpricing in this environment will cost you time and ultimately money. If you are weighing whether to sell, my seller net sheet calculator will give you a realistic picture of your proceeds after commissions, transfer taxes, and closing costs. And if you are thinking about the cost of staying put versus selling, the opportunity cost calculator can help you think through that decision with real numbers.

Looking Ahead

The FOMC meets April 28-29, and while no rate change is expected, the statement language and press conference will be closely watched for any shift in tone around future cuts. Also, a leadership transition at the Fed, with Chair Powell’s term expiring May 15, could add another variable later this year. The April jobs report arrives May 8, followed by the April CPI on May 12. If energy prices stabilize following the Iran-U.S. ceasefire declared in early April, the March inflation spike could prove to be a one-month anomaly rather than the start of a new trend. That distinction will shape the Fed’s thinking for the rest of the year.

Whether you are buying, selling, or just trying to make sense of the market, I am always happy to talk through what these numbers mean for your specific situation. Reach out anytime at megan@meganmicco.com, (510) 708-9952, or through my website.